How much do Medicare supplement plans cost per month is the usual question that agents get when it comes to the top 3 Medigap plans. In the video I show a 65 year old pays on average of $140 for a plan g, $106 for Plan N and $40 for a plan HDG.

A Medigap plan is a private insurance plan that helps cover costs that are not covered by Original Medicare deductibles, coinsurance, and copayments. Medigap plans are offered by health insurance companies such as Aetna, Cigna, and Humana. Plans are identified by letter – for example, the “G” plan or the “N” plan. Each lettered plan differs in its coverages. As a Medicare recipient, you do not have to purchase a Medigap plan. But without them, you may face high costs for hospital admission and doctor’s visits as some of these fees may not be fully covered by original Medicare.

Medigap plans are also known as Medicare supplement plans, supplemental Medicare plans, and Gap plans. This can cause some confusion when you are looking at different kinds of plans. An easy tip – Medigap plans have a letter associated with it – for example, G plan or Plan G.

Since Medicare Part A and B do not cover the full cost of health care, it is important to consider another way to cover out-of-pocket costs. Typically, Medicare Part A and B cover about 80% of the cost of hospital care and doctor’s visits. A Medigap plan covers some of the costs that remain – it may even cover the full cost, so you may pay $0 out of pocket when you have surgery or another procedure.

Medicare is your primary medical coverage. A Medigap plan, if you choose to purchase one, will be considered your secondary medical coverage. Medicare will be billed for your doctor’s visit or a health-related procedure. After Medicare submits payment for your visit or procedure, your health care provider will bill your Medigap plan for the remaining amount (the costs not covered by Medicare). Medicare supplemental plans (Medigap plans) are NOT the same, so your out-of-pocket costs will vary depending on the plan you select.

Are there really 10 Medigap Plans for 2023?

Many people review the Medigap plans available to them and find themselves asking many questions. It can be confusing! Part of the problem is that of the 10 plans, most people select either Medigap Plan G or a Medigap Plan N. Only 10% of the people purchase the other plans. Another important thing to know is that in 2020, Medigap Plan F is no longer available. Those who were eligible for Medigap Plan F prior to January 1, 2020, could keep their plan or switch to another company for the same Plan F coverage.

Another option you have when choosing a Medigap plan is the company you choose to purchase the plan from. So, you can choose your letter plan (for example, Medigap Plan G) and then choose the health care insurance company that will provide you with coverage for that plan (for example, Aetna or Humana). Keep in mind that Medigap plans are standardized government plans. This means that every company selling Medigap Plan G is selling the same Plan G. So comparing Plan G’s across different companies is like comparing “apples to apples”. However, the cost of the same plan differs across companies. So a Medigap Plan G purchased from Company A can cost you more than the same plan from Company B. So here is the trillion-dollar question: “Why would I purchase the plan from Company Q when the same plan from Company X is less expensive?” The answer is because we are all different. Some people want to purchase a plan from a large company like Aetna regardless of the cost while some people don’t care about the company as long as the cost is lower. REMEMBER that companies offer the same coverage for Plan G (or any other Medigap plan) regardless of the cost.

Now let’s talk about the two most popular Medigap plans:

Medigap Plan G

Medicare supplement Plan G is the most comprehensive Medigap plan in 2022. After Medicare pays its share of the bill, Medigap Plan G will cover everything else except the Medicare Part B deductible. The Part B deductible is $203 in 2021, but my guess is it will go up by 3% a year indefinitely. Let me give you an example. With Medicare coverage and a Medigap plan G from any company, open-heart surgery, hip replacements, stints, emergency room visits, etc. is covered at 100%. You will only have to pay the Part B deductible for outpatient care such as doctor’s visits. Imagine having open heart surgery and paying $0. That is Medicare Plan G.

Medigap Plan N

Medigap Plan N is the second most popular Medicare supplemental plan available today. With the Medigap Plan N, you will pay the Medicare Part B deductible which is $203 per year. In addition, with Medigap Plan N, you will also pay a copay up to $20 each time you visit a doctor or outpatient center. This can get expensive if you are receiving any kind of outpatient treatment a few times a week. For example, you could be paying $20 for each physical therapy visit and $60 if you have physical therapy three times a week. The copayments can add up. Another copayment that you will be responsible for under the Medicare Supplemental Plan N is the $50 emergency room copayment (unless you are admitted into the hospital). Lastly, some doctors charge an excess amount that the Medigap Plan N doesn’t cover. In some states, some doctors are allowed to charge 15% above the Medicare-approved amount. Less than 2% of the doctors in the US charge this excess charge, so I wouldn’t be alarmed – but it is information that you should know when considering Medigap Plan N.

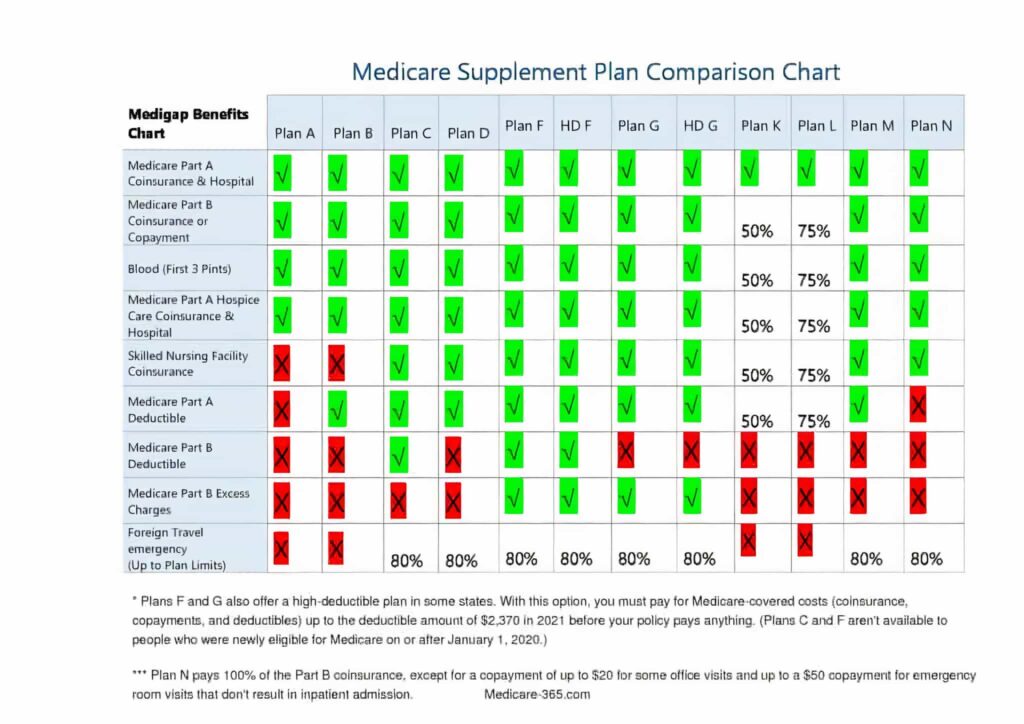

Compare Medigap Plans

Comparing Medigap Plans

There are a total of 10 Medigap plans to choose from in the year 2021, with Plan F now taken off as one of the options. Every plan has its own coverage as to what gaps in Medicare they cover. Using our chart below, you can compare all the plans together to see what fits your needs.

Each and every year the Medigap plan is updated to give you the most relevant and new information pertaining to your Medigap plan. Granted, most of the plans listed do not receive benefit changes throughout the years.

Depending on the Medigap plan, some have higher premiums than the others, but because of those high premiums, they give you more coverage.

Some of the Medigap plans that have a low premium mean you agree to the terms of the plan and will also pay for certain gaps within Medicare by yourself. Comparing the plans will give you a good idea as to what will cover your needs.

Medigap Insurance

Medicare Supplement plans or (Medigap plans) for short, are there to pay for gaps within Medicare. They can help pay for copayments, coinsurance, and deductibles.

Which Plan is Better?

Plan G is one of the most highly bought plans out of all the Medigap Plans. It used to be Plan F as well, but that was retracted back in 2020 and taken off the list of plans.

Since Plan F is no longer an option, Plan G is the go-to plan since it has almost every single benefit Plan F had with one difference. That difference is the Part B deductible is NOT covered in Plan G. You will have to pay that deductible on your own.

However, Plan N is on an uprise due to low premium costs. So if you can afford to pay out-of-pocket for some of your Medigap costs and excess charges then Plan N might be something to look into.

Medigap Chart and Summary of Parts

Medicare Supplement Plan A: Plan A is the most simplistic out of all the other plans. It will cover 20% of what Medicare does not cover on outpatient treatments. All Medicare Insurance companies have Plan A as an option, but depending on where you reside, some companies will not offer it to those below the age of 65 that are on Medicare Disability.

Medicare Supplement Plan B: With Plan B, this covers all of what Plan A covers except it will also pay the hospital deductible that Medicare Part A has. Medigap Plan B differs from Medicare Part B so make sure you do not confuse the two.

Medicare Supplement Plan C: This plan will cover everything aside from Medicare excess charges. It will pay the deductibles as well as the 20% usually paid by you towards outpatient costs.

Medicare Supplement Plan D: Plan D will not pay for the Part B deductible or excess charges on Medicare if they are incurred. Plan D is one of the unpopular plans within Medigap. It is not Part D in Medicare which is the Drug Plan.

Medicare Supplement Plan G: Plan G covers everything that Plan F covered when it was available, except the Part B deductible. Since Plan F is no longer around, Plan G has become one of the most popular plans found around the states.

Medicare Supplement Plans K, L, M: The plans K, L, and M are not widely requested because of the amount they cover. With Plan K, it will only cover half or 50% of things, while Plan L will cover ¾ or 75% of things. Since the request for these plans is low, not many insurance companies or carriers will offer them. Depending on where you are residing, you may have a good chance of finding decent rates for the plans.

Medicare Supplement Plan N: Plan N which was made back in 2010 or a little over a decade ago, has low premiums yet you pay out-of-pocket for copays pertaining to visits with a doctor and emergency rooms. Plan N will not cover excess charges incurred within Medicare.

Medigap Plans and Doctors

With Medicare Supplement Plans you are able to visit any doctor for a checkup as long as they are within Medicare. If the doctor accepts Medicare, you are then eligible to go and visit him/her for a checkup. It will not matter what company you choose to get your plans from. Medicare Advantage plans are where you are limited to a network of doctors, but Medigap is not the same.

Medigap Open Enrollment

In most cases, enrolling in a Medigap policy during your open enrollment period is the best option. You have a six-month open enrollment period under federal law, which starts 3 months prior to you turning 65, the month you turn 65, and 3 months after. This is when you enroll in Medicare Part B (very important).

While your enrollment period is open, Medigap firms have to sell you a policy at the simplest offered rate notwithstanding your health status, and coverage cannot be denied to you. The ideal rate may rely upon a variety of factors. For example, age, gender, marital status, and zip code. If you get a Medigap plan while your enrollment period is open, policies are restricted in their ability to exclude coverage for pre-existing conditions.

Guaranteed Issue Right

Be sure not to miss out on your open enrollment period. If you do, but have a guaranteed issue right, however, you are still eligible to purchase a plan. Once you turn 65 or are older than that a guaranteed issue right is available to you if you have certain health coverage that is no longer covering you or stop your health coverage.

With a guaranteed issue right, Medigap firms have to sell you a policy at the simplest offered rate notwithstanding your health status, and coverage cannot be denied to you. The ideal rate may rely upon a variety of factors. For example, age, gender, marital status, and zip code. If you get a Medigap while your enrollment period is open, policies are restricted in their ability to exclude coverage for pre-existing conditions.

On another note, you may also have a guaranteed issue right if these circumstances apply to you;

- A group healthcare plan that was covering your Medicare cost-sharing was lost, but you played no role in it falling through.

- Were accepted into a Medicare Advantage Plan right when the enrollment period opened for you but was then unenrolled within a year from acceptance.

- The current Medicare Advantage Plan or Medigap policy decides to end their coverage or commits a felony.

Purchasing a Medigap policy if you missed the enrollment periods

If you have missed out on the enrollment periods yet still want to purchase a Medigap policy when the enrollment windows are closed here is what to be aware of. The companies that are offering the policies can choose not to sell you one or may require that you have specific medical requirements. Let’s say a company decides to sell you a policy, a high monthly premium may be applied that you will have to pay on top of a half-year waiting period you have to wait before they will cover the pre-existing medical conditions.

Plan G Vs Plan N

Those already enrolled in Medicare Part A and B have the option to look for additional coverage from a Medigap plan. The two biggest Medigap plans are Plan G and Plan N.

Plan G and Plan N Similarities

First let’s breakdown what Plan G and N have in common:

- Both have Medicare Part A deductible coverage, meaning you do not have to pay for the deductible.

- However, the Medicare Part B deductible which is $203 is not covered by these plans.

- If you are in need of care from skilled nurses at a facility, hospitalization, hospice, or travel to foreign places, you are covered with these plans.

- In order to apply the application goes through underwriting UNLESS you enroll during an open enrollment period or are in a guaranteed issue circumstance.

How Each Plan is Different

Plan G:

- Does not have copays for Part B doctor or outpatient visits

- No copays for the emergency room

- Excess charges for Part B cannot be more than 15%. The 15% is the price difference from services covered by Medicare and how much the health care facility is charging.

Plan N:

- There is a copay for Part B that can be as much as $20 per visit to a doctor or outpatient care.

- If you visit the emergency room then it can be a $50 copay with Part B, unless you were admitted into the hospital then that fee is waived.

Medigap Plan G & Plan N Premium Differences

The Plan G premium is $20 to $30 more than the Plan N premium throughout most of the states in the U.S. Reason is there are no copays for visits to the doctors or outpatient care unlike with Plan N. Keep in mind that each state might have different prices for premiums for example, in Tampa, Florida premiums might be only $20 for Plan G while somewhere like Philadelphia, Pennsylvania may have a $25 premium.

Plan F Explained

With Plan F those who are turning 65 in the year 2021 will not be able to apply for it. Plan F was taken off Medigap in 2020, but those who were already on the plan before it was gone do not have to worry. Anyone currently on a Plan F can stay on the plan and can even switch between other Plan Fs if the one they are on now is too expensive. However, if they decide to switch they will have to go through underwriting to see if they are eligible to switch.

Medigap Companies

There is a multitude of Medigap companies out in today’s Medicare market. From brand-named companies to ones that are less known, they all have something in common. That similarity is all these companies offer the same coverage whether it is from a big-name brand or a smaller brand.

Standardized Medigap Plans and Benefits

The Medigap plans offered by any Medicare Insurance company all work the same way. A Plan N at somewhere like Aetna is a Plan N nonetheless. One difference is that depending on the carrier of these plans, the prices will be higher or lower.

Choosing a Medigap plan really relies on what type of coverage you need as well as what you are able to afford price-wise. Let’s say company A has a Plan G you want to be on priced at $150 a month. On the other hand company B, the lesser-known company has the same Plan G, but it is priced at $130. At this point, it is up to you to decide whether you would like to pay $150 for a big-name brand company OR choose the smaller company and only pay $130.

Name Brand Medigap Insurance Companies

Most citizens on Medicare, are more comfortable picking a company whose name they are very familiar with since it brings a sense of security along with it. There are other companies offering the same things, although due to the fact that people are unfamiliar with them and know too little about the company, they feel unsafe choosing the smaller company.

In the end, it is up to you the buyer to pick what you feel the most comfortable with whether it’s a brand-named company or a small one. Speaking with a Medicare Supplement agent will help in deciding since they are more versed in the knowledge of Medigap plans and the companies that offer them.

Medigap Vs Advantage Plans

These two policies both cover gaps within Medicare, yet work differently in doing so.

Medigap (Medicare Supplements)

For Medicare supplements, they pay once Medicare has paid for their share of a bill. If you are on Medigap you are still on Original Medicare. Whenever a bill is received from any health clinic, doctor, hospital, etc. Medicare covers whatever they have to and any excess is then sent to the Medicare Supplement company you have chosen. Depending on the plan taken with the Medigap company depends on how much the company will pay towards the bill.

Medicare Advantage

Medicare Advantage plans are a separate entity from Medicare. Benefits come from your Advantage plan rather than from Medicare itself. Within the Advantage plan, you use the network providers from an HMO or PPO plan unless it is an emergency. Also, copays are expected to be paid by you for health care.

Supplement Plans Continued

Medicare supplement plans as stated before are secondary to your Original Medicare. With Medigap, any Medicare provider is available to you without needing a referral. Enrolling in a Plan G with saving on out-of-pocket costs and doctor copayments. Once you have enrolled in a Medicare Supplement plan, Medicare is then notified of your purchase and any bills not fully taken care of by Medicare are handed off to the company you chose to pay the rest off. The supplement plans allow one to go to any hospitals or doctors in the U.S. Not only that, a referral will not be needed either to see a specialist. That being said, the plans’ premiums are higher than a Medicare Advantage plan.

The Medigap plans will cover drugs that have been given in a hospital/clinic area, but will not cover prescribed medications outside of the hospital setting. Most clients enrolled in a Medigap plan end up paying for a separate Part D drug plan in order to have coverage for prescription drugs.

Don’t forget, enroll during your open enrollment window which is from the start of your Part B Medicare effective date and six months after to be approved with no health questioning.

Medicare Advantage

Medicare Advantage policies are private insurance plans which can have low premiums compared to Medigap plans and even the possibility of a $0 premium.

Part B premiums are paid for on a monthly basis by you and you have to be on Medicare Part A and B for eligibility to get on a Medicare Advantage Plan. A $0 premium plan usually means that the network providers for the plan have less doctors to choose from when comparing it to a Medigap plan. Plus the insurance company controls the choice of providers given to you.

If you already have a doctor you go to for checkups, check to see if they are within the network of the plan you are looking at. The HMO plan has a small network so if you choose this be sure to double-check and see where you would have to go for checkups if the primary care physician you go to is not in the network.

The insurance companies that sell Medicare Advantage Plans pay for the healthcare bills rather than Medicare itself paying for them. If you are on a Medicare Advantage plan then you pay the copays that come from the services you use within the network.

Only one health question is on a Medicare Advantage application and that is if you have End-Stage Renal Disease which would disqualify you from obtaining Medicare Advantage plans. In the year 2021, there are no questions pertaining to health on any Medicare Advantage plan applications.

Most Medicare Advantage plans do come with a Part D drug plan attached so unlike Medigap you do not need to purchase a separate drug plan. Be sure to check and make sure there is a Part D attached, on the off chance it is not you need to talk with a Medicare Supplement agent to see what the next steps to take are.

There is a maximum out-of-pocket policy in place on all Medicare Advantage plans to protect you from spending too much. As of 2021, the maximum limit cannot be higher than $7,550.